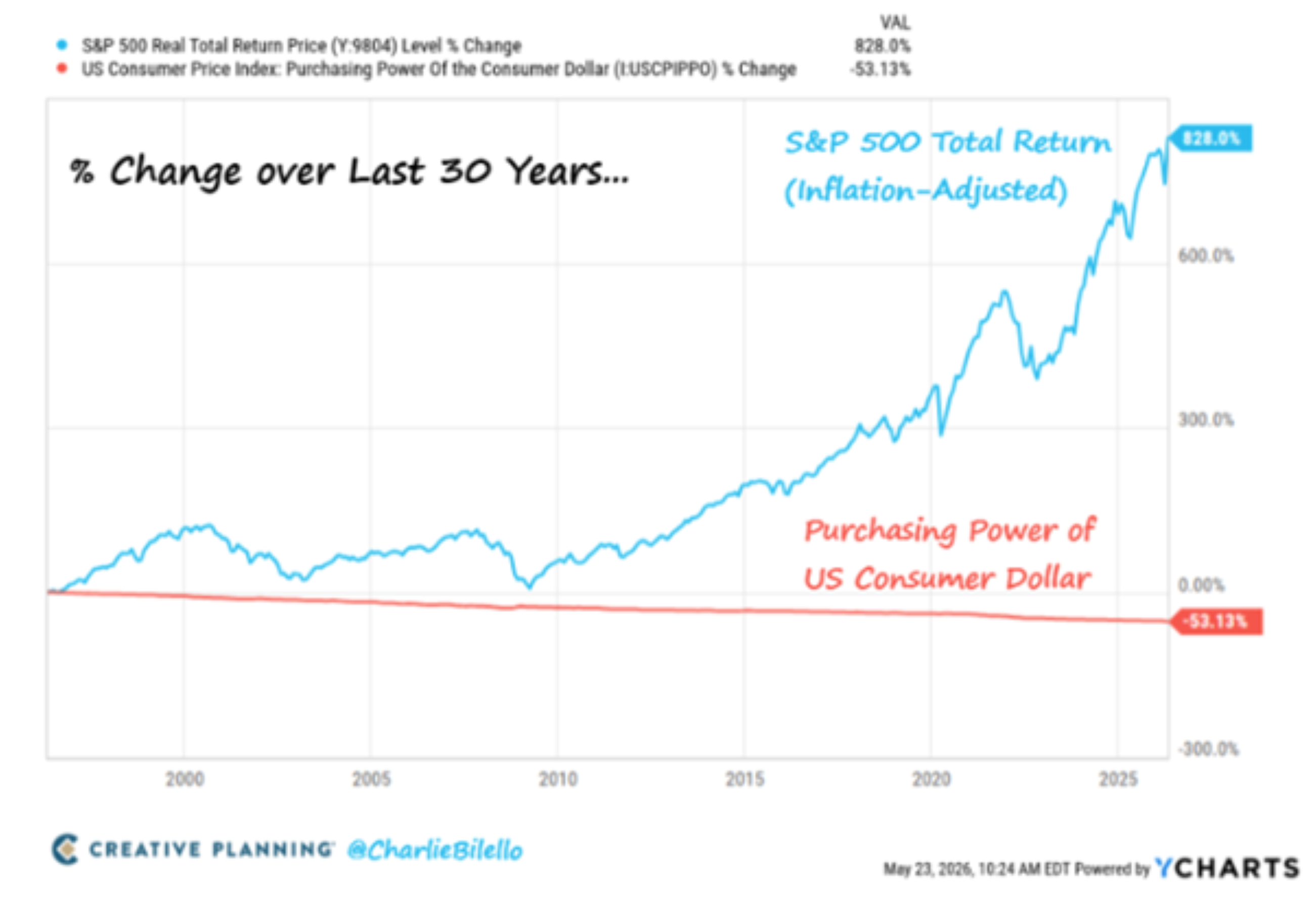

COLUMN - Over the last 30 years, the purchasing power of the US dollar has been cut in half by inflation.

A dollar in 1996 buys roughly 50 cents worth of goods today.

Over the exact same period, the S&P 500 gained 828%. And here is the part that matters: that is after adjusting for inflation. In real terms, after the silent tax of rising prices has been stripped out, American equities returned 7.7% per year for 30 years.

That is the entire case for investing in growth assets, in one chart.

Not because markets go up every year. Not because shares are always comfortable to own. But because over long periods, cash quietly loses purchasing power, while productive assets have the ability to grow far ahead of inflation.

I wanted to see what the equivalent looked like in South Africa, so I ran the numbers myself. Treat these as estimates, but the picture is clear.

Our inflation story is actually worse than America's. A basket of goods that cost R100 in 1996 costs around R470 today. The rand did not lose half its purchasing power. It lost nearly 80% of it.

The JSE All Share Index grew from around 6,200 points to roughly 115,000 over the same period. If we add a rough dividend assumption of around 3% per year, the total nominal return works out to roughly 12 to 13% per year.

Strip out 6% inflation and you are left with approximately 6% per year in real terms. Over 30 years, that compounds to around 500%.

Less than the American number, yes. But still a fivefold increase in real purchasing power through currency crises, load shedding, political noise, and two major global market crashes.

This matters especially in retirement. Retirement is not a short-term problem. For many people, it is a 20 or 30-year investment period.

Many retirees naturally want safety, and that is understandable. But there are two types of risk. The first is market risk, the risk that your portfolio falls in value from time to time. The second is inflation risk, the risk that your money holds its nominal value but slowly loses its ability to fund your life.

Market risk is visible. You see it on your statement. Inflation risk is quieter. You feel it through medical aid increases, insurance premiums, groceries, school fees and the cost of replacing a car.

That is why a well-built portfolio needs both safety and growth. The safer assets fund short-term income needs and reduce the need to sell growth assets at the wrong time. The growth assets make sure the portfolio still has a chance of funding your life 10, 20 or 30 years from now.

The goal is not to avoid all volatility. It is to structure the portfolio so you can live with the volatility, while keeping enough exposure to assets that have historically beaten inflation over long periods.

Because the real risk is not just that your portfolio falls. The real risk is that your money stands still while the cost of your life keeps moving.

Matthew Matthee has a wealth management business that specialises in retirement planning and investments. He writes about financial markets, investments, and investor psychology. He holds a Masters Degree in Economics from Stellenbosch University and a Post Graduate Diploma in Financial Planning from UFS. [email protected]

‘We bring you the latest Garden Route, Hessequa, Karoo news’